Recent Trends in Securities Class Actions & Introduction of Emerging Firms, 2006-15

NERA and Cornerstone have recently published annual reports showing that the volume of securities class actions has increased from 2006 to 2015, with a low in 2009 and a steady rise since then. In this blog we use the more detailed data of the SSLA database to dig deeper into this trend and expose some interesting drivers. As we will explain, the increase in case volume has come with a decrease in average case quality, measured a few different ways. In addition, low quality cases appear to have been litigated disproportionately—though not exclusively—by a group of firms that until 2009 had a relatively small share of the federal securities class action market but whose share has increased substantially since then. Much of the data we provide here will be presented in charts, with relatively little text. For a more detailed discussion of the data, please see our post on Kevin LaCroix’s D&O Diary blog.

[NOTE: Mousing over the elements of each chart below will reveal more data. Clicking the chart legends will hide (empty circle) or show (full circle) specific data categories.]

Figure 1: Filings by Year

Figure 1 shows the annual volume of securities class action filings from 2006 to 2015 with a breakdown of those cases into those involving allegations of financial misstatements and those involving allegations of only non-financial misstatements. Financial misstatements are misstatements in a company’s financial statements. Non-financial statements are all other misstatements, which as explained below, can have a financial element as in the case of overly optimistic financial projections. This distinction and the large increase in non-financial cases is a central theme in the explanation that follows.[1]

Dismissal Rates

Figure 2a: Dismissal Rate by Resolution Year

Figure 2a shows a rising dismissal rate since 2006, especially since 2008. Most of the dismissals occur in non-financial cases which, as shown in Figure 1, have increased.

Figure 2b: Dismissal rates between financial and non-financial cases

Figure 2b shows the dismissal rate for all types of cases was higher in the second half of the 2006-2015 decade than in the first half. The dismissal rate for non-financial cases increased from 63% to 56%. Since these cases increased the most in volume, dismissals of non-financial cases accounts for a large share of the overall increase in the dismissal rate over the decade.

Figure 3a: Nature of Alleged Misstatements in Non-Financial Cases

Figure 3a focuses on non-financial cases to pinpoint the nature of their weakness in more detail. The most common type of non-financial cases are those involving missed earnings and those involving statements about products or operations. Both missed earnings cases and product and operations cases accounted for most of the increase in non-financial cases over the 2006 to 2015 period.

Figure 3b: Dismissal Rates by Alleged Nature of Misstatements

Figure 3b shows that dismissals of both missed earnings cases and product and operations cases increased substantially over this decade—from 52% in the first half of the decade to 64% in the second half. During this same period, the dismissal rate for other nonfinancial cases actually declined slightly.

Figure 4: Targeting Technology and Healthcare Companies in Non-Financial Cases test

Figure 4 shows that from 2006 to 2015, healthcare and technology companies have been targeted with increased frequency. Dismissal rates for cases against companies in these sectors have also increased in the second half of the decade in in both non-financial cases and financial cases).

In sum, both the increased volume of cases and the increased rate of dismissal over the 2006 to 2015 period is largely explained by a change in the composition of the cases toward more non-financial cases, and more specifically, missed earnings cases and product and operations cases, largely in the technology and healthcare industries. The related trends of higher volume and lower quality cases raises the question why plaintiffs’ law firms are filing these relatively low quality cases.

Emerging Plaintiffs Law Firms

Figure 5: Emerging Firms as Lead Counsel

Figure 5 shows a pattern that may at least in part explain the increasing volume of filings and the increased dismissal rate over the past decade Beginning in 2009, a group of plaintiffs’ law firms that we will call “emerging firms”[2] increased their volume of cases substantially, in both absolute and percentage terms.[3]

Figure 6: Change in Filing Volume Between Periods 2006-10 and 2011-15

Figure 6 illustrates the role of emerging firms in the increase filing of cases alleging non-financial misstatements in absolute number and as a percent of total filings between 2006 to 2015. Plaintiffs firms that have maintained a high volume of cases throughout the past decade—a group of firms we will refer to as “established firms”[4]—increased their targeting of non-financial cases by 16% (25 cases), while emerging firms increased their filing of non-financial cases by 396% (95 cases). Moreover, among the non-financial cases, emerging firms filed a disproportionate number of cases alleging missed earnings and cases alleging product and operational problems—the types of cases shown above to account for both the increase in case volume over the decade and the increase in dismissals.

Figure 7: Dismissal Rates of Established and Emerging Firms

Figure 7 shows that cases filed by emerging firms have been dismissed at a higher rate than cases brought by the established firms, and that the dismissal rate for emerging firms increased as the volume of their cases increased from the first to the second half of the decade.

Figure 8: Settlement Timing by Firm Type

Figure 8 compares settlement timing for emerging firms to that of established firms. During the entire 2006-15 period, 22% of cases settled during early pleading—before the ruling on the first motion to dismiss. Emerging firms settled disproportionately early compared to establish firms.

Figure 9a: Median Settlement Size by Timing

Figure 9b: Mean Settlement Size by Timing

Figures 9a and 9b show that the settlements the emerging firms reached at this early stage were relatively small. The size of settlements reached during discovery are also dramatically different between emerging firms and established firms.

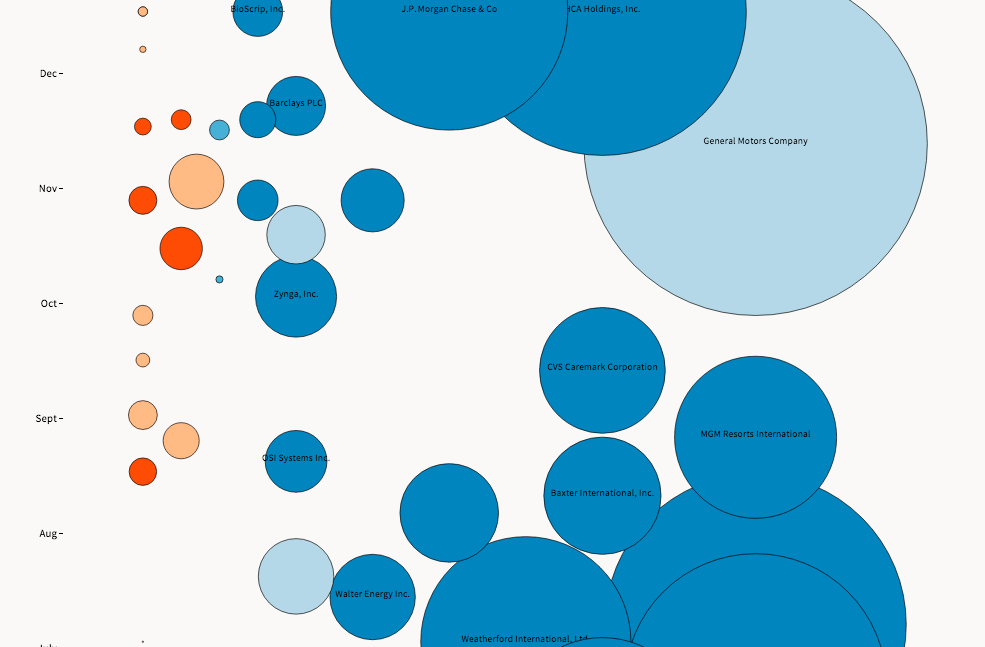

[NOTE: Click the image on the left to view the full, interactive chart]

Figure 10 illustrates the differences between emerging firm and established firm settlements reached in 2015 alone. This chart shows settlement size by relative area of the circles. The shade of color for each circle represents settlement timing, with the lightest shades representing cases that settled during early pleading and the darkest shades representing cases that settled during discovery. Clicking on the chart will take you to a separate webpage with a larger version of the chart. On that webpage, rolling over a particular settlement will reveal additional information collected by Stanford Securities Litigation Analytics about each case. A link at the top of that page will return you to this blog post.

Conclusion

In sum, there is more than initially meets the eye in the increase in the volume of securities class actions over the past decade. This increase in volume has been associated with an increase in dismissals and other indicators of low quality cases, which in turn is linked to a change in the nature of the lawsuits that have been filed between the beginning and end of the decade. Cases involving only non-financial misstatements are the source of the increased volume—specifically cases alleging misstatements related to missed earnings and product and operational matters, largely in the healthcare and technology sectors. This new set of cases have been filed by firms that we have termed “emerging firms”—firms that increased their filings and their share of the securities class action market over the course of the past decade.

[1] If we were to include merger objection class actions brought under Section 14(a) of the Securities and Exchange Act, the pattern would be the same, with 209 cases in 2015 compared to 170 for example, but the analysis would be unchanged.

[2] These firms were The Rosen Law Firm, Pomerantz LLP and Glancy Prongay & Murray LLP. The firms with the next largest increase in volume were Kahn Swick & Foti LLC, Scott & Scott LLP and Motley Rice LLC, but these firms had less than one half volume of lowest volume “emerging firm” over the same year period, and with annual filing numbers declining from 2006 to 2015.

[3] Among cases where lead plaintiff and lead counsel have been appointed.

[4] Established firms are defined as the top 10 in lead counsel volume from 2000 –2015 and at least 5 settlements on the Institutional Shareholder Services Top 100 Settlements list. The following firms meet that definition of “established”: Barrack Rodos & Bacine, Berman DeValerio, Bernstein Litowitz Berger & Grossman LLP, Grant & Eisenhofer P.A., Kaplan Fox & Kilsheimer LLP, Kessler Topaz Meltzer & Check LLP, Kirby McInerney LLP, Milberg LLP, Labaton Sucharow LLP and Robbins Geller Rudman & Dowd LLP.